Housing affordability in the Waikato remains structurally constrained, with significant implications for regional productivity, wellbeing, and economic resilience. Despite increased housing supply (~20,000 homes over five years), only ~1% has been affordable, indicating that current system settings are not delivering accessible outcomes—including for middle-income households. Our more recent State of the Region Report[1] further reinforces the role of affordable housing in wellbeing and family prosperity.

With WHI and others in 2025 we asked the question “what would it really take to make housing affordable in the Waikato”. We commissioned Veros Ltd. to:

Identify and advance real world solutions on what it would take to improve housing affordability in the Waikato region.

Develop a practical, data-driven Investment Model that identifies commercially feasible pathways for delivering affordable rental and ownership housing to middle-income households (earning $60,000–$150,000 annually) in the Waikato region.

Develop actions grounded in what is commercially feasible for the private, community/for purpose and iwi development sectors.

Be actionable, understandable, and relevant to the development community, adaptable across a range of settings and be focused on land that is development ready.

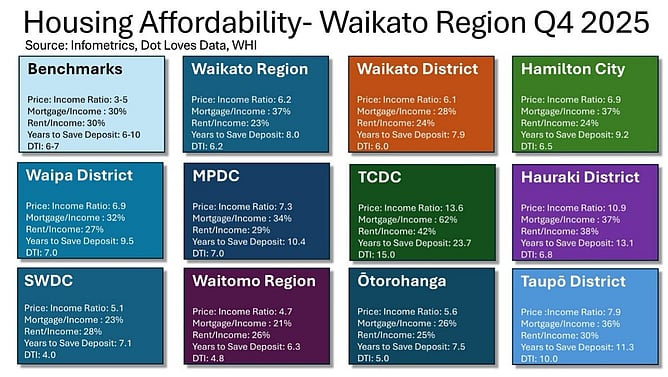

Housing affordability measures often used include income: price ratios, percentages of income needed to service a mortgage or rent, years to save a deposit and more recently debt to income ratios. Such statistical approaches are illustrative of overall system performance, although they can result in anomalies- for example in areas with lower that average median incomes but high house prices- such as the Coromandel Peninsula, or areas undergoing rapid gentrification. Latest data from Infometrics, Waikato Housing Initiative and Dot Loves Data in Figure 1 shows the following affordability indicators by district for the Waikato region:

Price to income ratio

Mortgage affordability (% of income needed to service a mortgage)

Rental affordability (% of income needed to pay rent)

Years to save a deposit (years needed to save a 20% deposit based on saving 10% of income, with an allowance for rent already being paid)

Debt to income ratio (Reserve Bank debt limit).

Figure 1. Housing Affordability Indicators for the Waikato Region, Q4 2025

Figure 1 shows the affordability benchmarks used for the indicators, and the results for the districts in the Waikato region[1]. Across the region, most districts are at or above the upper levels of affordability for most of the metrics, with some (for example Thames Coromandel, Taupo and Hauraki) significantly above on Price:Income ratios and years to save a deposit. Others such as Waitomo, Otorohanga and South Waiakto are closer to the benchmarks.

At the district level, these summary statistics mask considerable variation at finer scales such as SA2[2]. Factors which affect housing affordability can vary significantly within a district at this scale including:

Deprivation

Income and employment

Percentage working age population/retirees

House price and rental

Connectivity

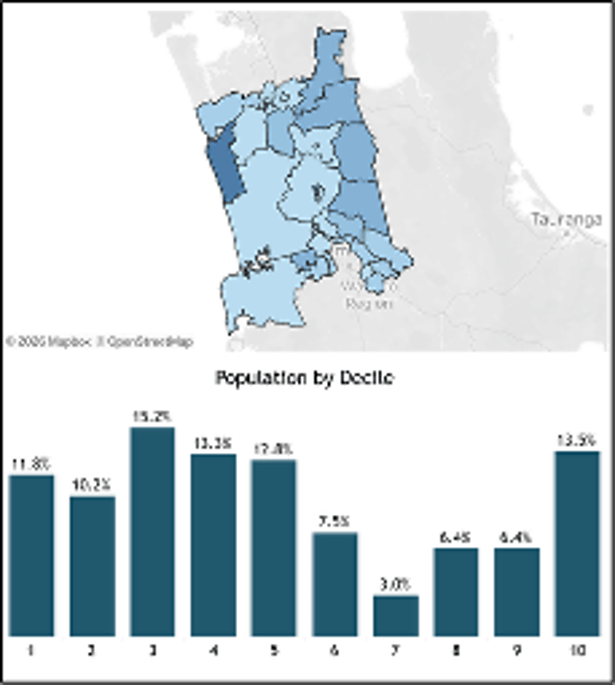

For example, within the Waikato District, deprivation ranges between Huntly West (Decile 9 -highest deprivation in district) to Horsham Downs (Decile 1- lowest deprivation in district) as shown in Figure 2. This materially affects housing affordability within different parts of the same district.

[1] Rotorua Lakes district is excluded only for legibility purposes.

[2] An SA2 area usually has a shared road network, shared community facilities, shared historical or social links and socio-economic similarities. In cities, SA2 areas are usually suburbs or part-suburbs with 2,000 to 4,000 residents. In rural districts, many SA2 areas have populations of fewer than 1,000 residents.

Figure 2. Deprivation in the Waikato District, 2023 (Census), WHI Housing Data Lake

The three summary insights from the work so far are:

A. Delivering Affordable Homes is like ‘Death by a Thousand Cuts’

The development process is long, uncertain, costly and risky. Every participant feels the impact:

councils managing complex consents

developers rezoning land

builders delivering new homes

people trying to subdivide their property.

Layers of red tape, risk-averse decision-making, and requirements for high-quality amenity and construction standards while essential for safe, healthy, and attractive neighbourhoods come at a significant cost to affordability. These processes add time, increase risk, and drive-up costs, ultimately reducing supply and worsening the affordability challenge.

B. Affordability Means Building Smaller, Smarter Homes

Over the past decade, the cost of a new home has surged dramatically. One example which is a three-bedroom standalone home shows a 130% increase, rising from $350,000 to $815,000, while the Consumer Price Index grew by just 35%. This gap highlights the scale of the affordability challenge.

Reducing prices is extremely difficult. There are significant wage growth pressures, material costs remain high due to reliance on imports and restrictive regulations, business expenses continue to rise, and complex processes add layers of cost and risk. These factors make significant price reductions unrealistic.

This means to deliver cheaper homes; we need to build smaller homes. However, these homes need to meet the requirements of different people because “one size does not fit all”.

A mix of typologies is needed, including granny flats, duplexes, townhouses, apartments, multi-generational homes and retirement villages. This will better meet the needs of everyone, particularly as our ageing population occupies larger homes that families need.

C. Buyer Mindset + Market Demand Matter

Housing costs have far outpaced wage growth, making the first home many hardworking Kiwis aspired to a decade ago unattainable. Prices are unlikely to fall significantly and is forcing buyers into homes they cannot afford.

Part of the solution sits with the buyer’s choice and education. We need financial literacy and a willingness to embrace affordable, smaller, smarter homes.

In delivering affordability in face of rising house prices ‘new builds’ become a powerful tool. On the demand side, most lenders require only a 10% deposit for new homes compared to 20% for existing properties. That’s half the time to save, and this speed can make the difference between getting on the ladder or missing out entirely, as house prices historically rise faster than incomes.

On the supply side, new smaller homes add much needed stock to help stabilise prices. But people need to want new homes and importantly understand how to buy them. Financial literacy and confidence in off-the-plan purchases will create the real demand developers need from lenders to deliver smaller, more affordable homes.

Actions Proposed

Strategic Response: Targeted, System-Level Interventions

Six integrated initiatives are proposed to address these constraints as shown below. More information can be found by using the QR code. At least half of these actions can be progressed relatively quickly and at very low cost by local government, particularly the Affordable Housing Handbook and Feasibility Calculator, which provide immediate decision-support and system alignment benefits.

The Pattern Housing Blueprint aligns with work already being advanced by central government, positioning the Waikato to act as an early regional leader in adopting and scaling standardised affordable housing typologies.

Figure 3. Affordable Hosing proposed Actions, 2026

Other initiatives such as the Housing Equity / Impact Fund—are more complex and will require further development. However, they are potentially high-impact interventions, with comparable approaches in Tauranga and Taranaki demonstrating their value. These are strong candidates to be progressed through the Waikato Housing Initiative (WHI) work programme for 2026-27.